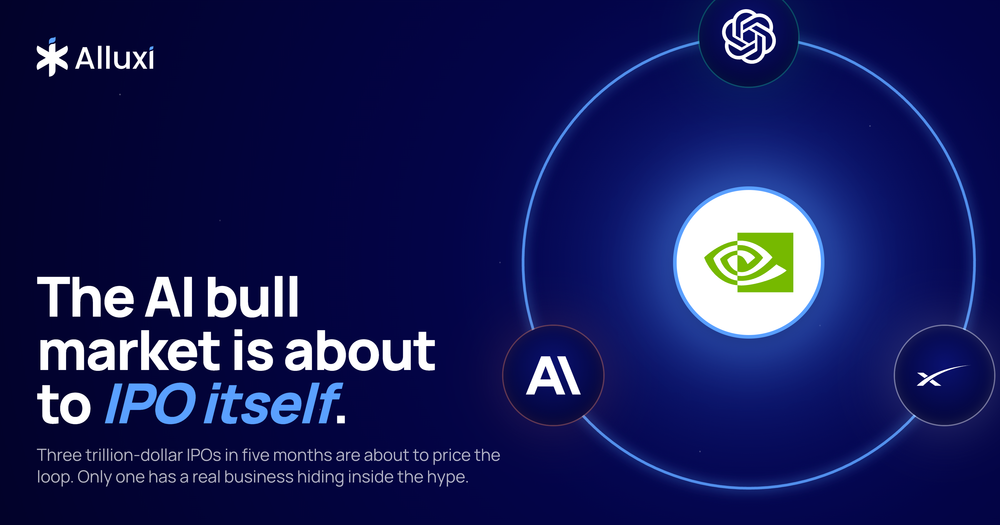

The AI bull market is about to IPO itself

Saudi Aramco's IPO held the record for the biggest in history for six years. SpaceX broke it on May 20, filing for nearly three times the size. Two days later, OpenAI filed its confidential S-1. Anthropic is right behind, closing a $50 billion bridge round this week ahead of an October listing already booked at Goldman.

Three companies. Five months. More new public equity than the entire 2024 IPO market combined.

Numbers like that line up only when the private market has run out of room to mark itself up, and the smart money wants to ring the register. Most retail coverage misses the part underneath.

Same money, four tickers

NVIDIA invests in OpenAI. OpenAI along the way the truckload for Colossus, the 220,000-GPU data center it spun up in 120 days. Anthropic pays SpaceX $1.25 billion a month to rent capacity on that same Colossus. NVIDIA also took a stake in Anthropic on the way through.

It's the same dollar bouncing through four ticker symbols, with NVIDIA clipping margin on every pass.

Each transaction is closed. The chips ship. The models train. The customers pay actual money. But every valuation in this loop moves together, because underneath the press releases, there's one flow of capital wearing four different costumes. When NVIDIA invests in OpenAI, OpenAI books revenue from the GPU spend, NVIDIA books revenue from chip sales, and both companies report growth. Looks like two businesses scaling from the outside. Looks like the same money counted twice from the inside.

Now three of those four are about to ask the public to fund the next leg.

The hidden utility

Inside the SpaceX prospectus is a number that makes the whole thesis more interesting.

Starlink reported $4.4 billion in operating income last year, with roughly 10 million subscribers paying around $120 per month. The legacy SpaceX launch business has carried more than 80% of the world's mass to orbit since 2023. Starlink is a profitable infrastructure company with a moat built into the physics. No AI required.

The $1.75 trillion ask doesn't sit on Starlink. Starlink alone is probably worth $200-$250 billion as a standalone business. The other trillion and a half is xAI, Colossus, and the orbital compute story Musk has been narrating since the February merger. SpaceX did $18.7 billion in 2025 revenue and posted a $4.9 billion net loss. Strip out xAI, and the rocket-and-satellite business is profitable. Add xAI back, and you have a ticker where the boring business pays for the speculative one.

OpenAI and Anthropic each have one product line, sold per token, with gross margins that compress whenever a competitor releases a model at half the inference cost. No Starlink underneath. OpenAI hit $25 billion in ARR in March and still lost $1.22 per dollar of revenue in Q1. Anthropic hit $19 billion ARR, up from $9 billion in January, against around $40 billion in committed GPU rentals over the next three years.

The numbers are growing. The unit economics are a different conversation.

Three founders, three bets

Musk is asking for $1.75 trillion while keeping 85% voting control through dual-class shares. He'll be CEO, CTO, and Chairman of SpaceX while still running Tesla. SpaceX opts out of Nasdaq's independent board requirements as a controlled company. Public investors get a ticker. Musk keeps the company.

Altman runs OpenAI through a Public Benefit Corporation whose largest shareholder is a nonprofit foundation with 26% and control rights. The S-1 will eventually have to explain how a board with a fiduciary duty to public shareholders coexists with a board with a fiduciary duty to safe AGI. The last time that question got asked seriously, in November 2023, it cost Altman the job for four days.

Amodei has the cleanest governance and the loudest enemy. Anthropic sued the Department of Defense in March after the DoD designated the company a supply-chain risk for refusing to let Claude be used for autonomous weapons or domestic surveillance. The company's own filings put hundreds of millions to billions of 2026 revenue on the line. A founder telling the U.S. government no, in writing, in a prospectus, is rare. Whether public-market investors reward it or punish it is the most interesting question in any of these three filings.

Around $135 billion of fresh public equity is about to pour into AI compute over the next twelve months. GPU prices fall. Inference costs fall. New models ship every quarter from teams that didn't exist eighteen months ago. The half-life of any product built on a specific frontier model is already shorter than a planning cycle.

The companies that win the next phase build like the model is already a commodity. The moat lies in domain knowledge, proprietary data, and workflow integration that no one outside your customers' walls can replicate. The boring layer outlives the shiny one, every cycle.

Three trillionaires get minted in the next twelve months. Probably four if NVIDIA holds. Whether any of it ages well depends on whether the loop still looks like a moat in 2028, or like a hall of mirrors.

The filings make the case. The next eight quarters will determine its price.